Economics Problems:

Economic

problem of mankind owes its origin to the fact that human wants are numerous and

of different kinds. The resources to satisfy the multifarious human wants are

limited

or scarce.

Diagram/Figure:

If the time or resources at our disposal

are unlimited so that we could satisfy all our wants, then no economic problem

would have arisen at all. Or If we had Aladdin’s lamp with us so that we could

satisfy all our wants by rubbing it, then there would have

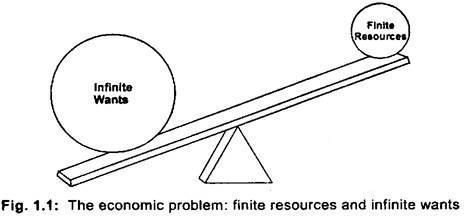

been no economic problem. The economic problem has arisen simply because as one

want is satisfied, another want appears on the scene. We can liken this to a

see-saw with on one hand the finite or limited resources and on the other hand

the unlimited or infinite wants.

As wants are unlimited and the means to satisfy them

limited, therefore, in order to get maximum satisfaction we are to choose our

wards by fixing up a list of priority. So the two foundation stones on which the

subject of Economics rests are:

(1) Multiplicity of human wants.

(2) Scarcity

of resources. This scarcity of means or resources creates two kinds of problems.

One is the allocation of resources to the best use so that the maximum

satisfaction is achieved. This can only be done if we arrange our wants in a

scale of preferences. Ordinarily, necessaries are satisfied first, comforts are

next and luxuries at the end.

The second problem is to eliminate waste. If in a

country the resources are not fully utilized and they are lying idle, this will

mean the maximum satisfaction is not being derived from the limited available

resources and being wasted for nothing.

The resources are not only scared but have

alternative uses. So a decided has to be made between them. The decision to make

choices between alternative uses has to be made by all of us. Even the richest

nation has distributed its resources in such a manner so as to be able to source

maximum satisfaction with minimum cost.

Importance of Economics:

Every economy has to solve the following five inter

related problems:

(1) What goods to be produce?

(2) How to produce?

(3) How to distribute income?

(4) How to ensure growth?

(5) Flow to ration the limited supplies?

These problems are now discussed in brief:

(i)

What goods to be produce? The first function

of the society is to decide which goods are to be produced and in how much

quantity. Since the resources at the disposal of the society are scarce, it

has to make a choice between “guns or butter”, or a choice between

necessities and luxuries. The decision about the allocation of resources

between consumer goods and capital goods; their quality and quantity is of

utmost importance from the point of view of economic growth.

(ii) How to produce? There are various

alternative methods or techniques of producing goods. The society has to

choose the least cost combination of producing the goods. For instance,

cloth can be produced with either handlooms (labor intensive technique) or

power looms (capital intensive technique). The society, depending upon its

resources and the state of technology available to it should use

the most efficient method of production.

(iii) How to distribute the national income?

The distribution of national income among the members of the community is a

burning issue both in the field of economics and politics. The socialists

are of the view that all the people should get fair share by redistribution

of national income. The other view is that, in a free enterprise economy,

each individual should get his share from the total output of goods

according to the income available to him through his genuine efforts.

(iv) How to ensure growth? The economic growth

can be attained by (a) increasing the rate of investment (b) replacement

of capital goods and (c) by improving the technical processes of

production, A society, therefore, shall have to take timely decisions for

allocating scarce resources for investment, replacement and technological

progress. In case a part of the resources are not diverted for capital

accumulation and technological progress, the rate of growth will go down.

The standard of living of the people will fall.

We, thus, conclude that economic problem arises

because of scarcity of resources that people want for the satisfaction of goods.

The scarcity of resources involves the problems of choice or allocation of

resources among the competing ends. Economics, in short, is a science of

efficiency in the use of scarce resources.

Relevant Articles:

|