There are various theories which have been put forward from time to time as

to why the interest is paid. The most important theories are:

(1) Productivity Theory of Interest.

(2) Abstinence or Waiting Theory of Interest.

(3) Austrian or Agio

Theory of Interest.

(4) Loanable

Fund Theory of Interest.

.

(5) Liquidity Preference Theory of Interest.

(6) Modern Theory of Interest.

Let us, now, examine these theories, one by one and see how they explain the

economic cause of interest.

(1) Productivity

Theory of Interest:

Definition:

Turgot and other physiocrats were of the opinion that interest is the reward

for the use of capital in production. Interest is paid, they say, because

capital is productive. The labor assisted by capital can produce more things

than what they can do without it.

Example:

For instance, a man with the help of

a machine can sew more clothes than without it. It is but Just and proper

therefore that a part of the pool of wealth which the capital has produced

should go to the lender of the capital. Interest is, thus, a payment for the

productivity of capital.

Criticism:

This theory has been severely criticized on the following grounds:

(i) This theory does explain as to why the interest is paid but it throws no

light as to how the rate of interest is determined.

(ii) According to this theory, interest is paid because capital is productive.

This means that pure interest should vary in proportion to the productiveness of the capital. But the fact is otherwise. Pure interest tends

to be the same in money market during the same period of time.

(iii) The theory only emphasizes as to why interest is demanded but it totally

neglects the supply side of the capital.

(iv) Finally, the theory fails to explain as to how interest is paid for the

loan borrowed for consumption purposes.

(2) Abstinence or

Waiting Theory of Interest:

Definition:

This theory of interest is associated with the name of Senior.

According to the theory:

"Interest is a reward for abstinence.

When a person saves

money from his income and lends it to somebody else, he in fact makes sacrifice.

Sacrifice in the sense, that he abstains from consuming the whole of his income

which he could have easily spent. As abstaining from consumption is disagreeable

and painful, so the lender must be rewarded for this. Thus, according to Senior,

interest is the reward for abstinence from the use of capital on the part of the

lender".

This theory is rejected on the ground that saving does not necessarily

involve discomfort or sacrifice. A millionaire may save and lend a major part of

his income without undergoing any hardship or suffering.

Marshall, Realizing this flaw in Senior's definition, substituted the term

waiting for abstinence. According to Marshall:

"Interest is the reward

for waiting. When a man saves a part of his income, he simply postpones his

present consumption to some future date. During a period when money is loaned,

he himself might stand in need of money. But he cannot get it back from the

borrower as the period of loan is fixed. He has to wait for the return of loan.

In order to encourage the spirit of waiting amongst the lenders, some inducement

is necessary and this inducement according to Marshall, is interest".

Criticism:

(i) The theory is criticized on the ground that it lays undue emphasis on the

supply side of the problem and ignores the demand side which is equally

important for explaining the economic cause of rent.

(ii) It is not true that all the money saved is only due to the inducement of

interest. Some persons may save money even if the rate of interest is zero.

(3) Austrian or Agio

Theory of Interest:

Definition:

The Austrian or Agio Theory of interest was first advanced by

John Rao in

1834 and later on, it was developed by the Austrian economist, Bohm-Bowerk.

According to Bohm-Bowerk:

"Interest is the premium or agio which present goods

command over future goods. The reason as to why present goods are preferred over

future goods are as follows:

Firstly,

Future is shrouded in mystery and so is uncertain. Secondly,

present wants are more urgently felt than the future ones. Thirdly,

present goods posses a technical superiority over future goods. Keeping in view

all the conditions stated above, an individual prefers present satisfaction to a

future satisfaction".

Example:

For instance, you give a choice to a

person either to have one bird which is in hand or two -in the bush. If the man is wise, he will

prefer the bird in the hand rather than two in the bush.

Take another example,

you give a choice to a man either to have $100 now or the payment of same

amount after, say, a year. The man if he is not a lunatic will prefer the

present payment. But in case you give the choice of the payment of $100 now

or $130 after six months, the man may be tempted to take $130 at the

future date provided he is satisfied that the extra payment of $30

compensates the sacrifice involved in postponing the present satisfaction.

Interest is, thus, the payment which a borrower has to make to the tender for

inducing him to put off the satisfaction of present consumption to some future

date.

Criticism:

The theory is criticized on the

following points:

(i) It attaches too much importance on the supply side of the problem and

ignores the demand side.

(ii) The theory does not throw light as to how the rate of interest is

determined.

(iii) It is also pointed out that interest is not paid merely because the tender

must be induced. The interest is paid because the borrowers are willing and able

to pay the loan.

(4) Loanable Fund Theory of Interest (Neo Classical Version):

Definition:

The theory was first put forward by

Wicksell and later on it was elaborated

by Ohlin, Robertson and Pigou, Myrdal etc. According to the neoclassical

economists:

"The rate of interest is determined by the interaction of the forces

of demand for loanable funds and the supply of it in the credit market".

We

briefly analyze the forces behind the demand for and supply of loanable funds

and then see how they interplay in the determination of the rate of interest.

(i) Demand for Loanable Funds: The demand for loanable funds comes from

households who need money for consumption purposes and from entrepreneurs who

require it for productive purposes. The total money borrowed by consumers for

consumption purposes forms only a small part of the total loanable funds, while

a major portion of the funds is borrowed by businessmen of all types. When an

entrepreneur borrows money, he keeps in mind two things:

(a) the expected net return on newly

invested funds, and (b) the

interest which has to be paid to the lender.

So long as the marginal efficiency of capital is above the interest rate, the

entrepreneur continues borrowing additional funds. When he finds that due to the

operation of law of diminishing returns, the marginal efficiency of capital has

fallen to the level of rate of interest, the entrepreneur stops borrowing

additional funds. Because if he invests more, the interest rate will be higher

than the marginal efficiency of capital and his profit will be adversely

affected. The last unit which an entrepreneur has thought worthwhile to employ

because the net revenue earned from it equals the prevailing rate of interest,

is railed marginal unit and its productivity as marginal efficiency of capital.

As all the units of capital employed are very similar and interchangeable to one

another in a competitive market, so the rate of interest which- is paid to the

marginal unit will also be paid to all other units. Thus, we conclude that on the side of demand, the rate of interest tends to be

equal to the, marginal efficiency of capital.

(ii) Supply of Loanable Funds: The supply of loanable funds comes from

savings by individuals, business concerns, discharging of idle cash balances,

bank credit. Disinvestment is another source of the supply of loanable funds.

All the sources of the supply of loanable funds are directly related to the rate

of interest. The higher the rate of interest, the larger is the supply of the

loanable funds and vice versa.

There is no doubt that higher rate of interest usually induces people to save

more but that is not always the case. There are people in the world who will

save even if the rate of interest is zero. But as their number is not very

large, so the savings of these people will not meet the demand for loanable

funds. Thus, rate of interest must be high to equate the supply of loanable

funds with the demand for it Let us now examine with the help of the following

imaginary schedule as to how the supply of loanable funds is adjusted to the

demand for it.

Schedule:

|

Demand for Loanable Funds ($1x10000000) |

Rate of Interest (%) |

Supply of Loanable Funds

($1x10000000) |

|

2

5

7

10 |

15

12

9

6 |

20

17

12

10 |

|

15

25 |

5

3 |

7

2 |

Diagram/Curve:

In this diagram (21.1) when the rate of interest is 6%, the demand for loanable funds is exactly equal to the supply of it. As the rate of interest,

which equals the demand for and supply of loanable funds is 6%, so the rate of

interest which will rule in the money market will be 6%. If the rate of interest

is higher than 6%, the supply of loanable funds increases more than the demand

for it. Competition amongst the lenders brings down the rate of interest to the

level of 6%.

If interest rate is lower than 6%, then the demand for loanable funds

increases more than the supply of it. Competition amongst the buyers

tends to raise the rate of interest. At 6% rate of interest, the total demand

for loanable funds is brought into equilibrium with the supply of loanable

funds. It is the rate which compensates the borrower as well as the lender.

Criticism:

The theory is criticized on the

following grounds:

(i) Unrealistic assumption: The theory assumes the level of

national income to be constant. Actually the level of income changes with

the changes in the levels of investment in the country.

(ii) Unrealistic integration of monetary and real factors: The

theory has integrated the monetary and real factors which affect the demand for

and supply of loanable funds. Actually both these factors are to be studied

separately and not to be combined.

(iii) Assumption of full employment: The theory assumes full

employment in the economy whereas less than full employment is the general rule.

(iv) Interest-elastic factors. The theory assumes that saving

hoarding investment, etc. are related to the rate of interest Actually

investment is not influenced by rate of interest alone. There are many other

factors also which affect investment in the country

.

(5) Keynesian Theory

of Interest/Liquidity Preference Theory of Interest:

Definition:

J.M. Keynes in his epoch-making book the General Theory of employment,

Interest and Money, has put forward a new theory of interest. According

to him:

"Interest is not the price for waiting. It is not the remuneration

necessary to call forth saving because a man may save money, bury it in his

backyard and get nothing from it in the way of interest. Interest is the reward

for surrendering liquidity, i.e., a reward for dispensing with the convenience of

holding money immediately available".

Example:

Just to make it more clear, we take an

example. Suppose, you lend a sum of $1000 to a person for six months in

return for a promise to get something extra in addition to the sum borrowed. If

the borrower returns you the same amount of money after six months, will

you be interested to part with or lend your ready money? Well, if

you are a philanthropist, then you may. But in case you are not, then

some incentive must be given to you for dispensing with the convenience of

holding money immediately available.

Interest is, thus, the reward for

parting with liquid control over cash for a specific period, or we say:

"Interest is the payment for parting with the advantages of liquid control of

money balance".

Here, a question can be asked as to why the need for liquidity arises

when people can earn interest by lending their ready money. Keynes has

given three distinct motives of demand for money or holding money in liquid

form.

(i) Demand for Money:

The main components of demand for

money are as under:

(a) Transaction motive.

(b) Precautionary motive.

(c) Speculative motive.

(a) Transaction motive. Transaction demand for money refers to the demand

for money to hold cash balances for day to day transactions. The transaction

motive relates to the desire of households and firms to keep a certain amount of

cash in hand in order to bridge the interval between the receipt of income and

expenditure. The transaction demand for money depends upon (i) size of income (ii)

time gap between the receipt of income and (iii) spending habit of the people.

Formula:

In symbols we can write:

L1 = F(y)

Here:

L1

is the transaction demand for money and F(y) shows it to be a function of income.

(b) Precautionary motive. The precautionary motive relates to the

desire of households and business concerns to hold a certain portion of the

total ready money in cash in order to meet certain unforeseen or unexpected

expenses like fire, theft etc. This demand for money depends upon (i) size of

income, (ii) nature of the people and (iii) foresightedness of the people.

As transaction and the precautionary

motives for holding cash depend upon income, as they are income elastic, Keynes

has put them together. It is expressed in symbols us:

L2

= F(y)

Which means that the liquidity

preference on account of the two motives called L2 is a function of

income.

(c) Speculative motive. The speculative motive relates to the

desire of the households and firms to keep a portion of their resources in ready

cash in order to take advantage of changes in the interest rates. If people

expect a rise in the rate of interest in the future, they will try to hold money

in cash in order to lend it in the future. Conversely, if they expect a fall in

the rate of interest, they will at once like to invest money now in order to

avail themselves of the advantages of high rate of interest. Thus, we find that

an expected rise in rate of interest stimulates liquidity preference and an'

expected fall has the opposite effect. It is written in symbols as:

L3

= F(r)

The liquidity preference for speculative demand for money

is a function of expected changes in the rate of interest.

We have discussed in all the three factors which exercise powerful influence

on the people's desire to hold money. The first two factors, i.e. the

transaction motive and the precautionary motive are not very much Influenced by;

the changes in the rate of interest, but the third factor, viz, speculative

motive is very sensitive to the changes in the interest rate. The major portion

of money which people want to hold in the form of cash infact is meant for

speculative purposes. When the rate of interest in a community is high, people

hold less money in the form of cash because by lending it to other, they earn a

sufficient amount of money. Conversely if the rate of interest is low, people

will not be very anxious to lend money. So the total money held by individuals

and business firms will be high. In short, the demand foe money to hold in cash

under speculative purposes is a function of the current rate of interest. It

increases as the interest rate falls and decrease as the interest rate rises. We

can say that demand for money for speculative motive is a decreasing function of

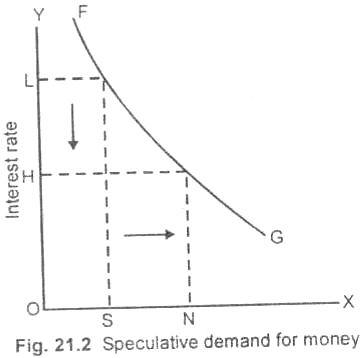

the rate of interest as is shown in the fig. 21.2.

Diagram/Curve:

In fig, 21.2, along OX is measured the demand for money which people want to

hold in the form of cash and along OY is shown the rate of interest. FG is the

liquidity preference curve which slopes downward from left to right. When rate

of interest is high, i.e. OL, the demand for money to hold in the form of ready

money or cash is OS only. When the interest rate falls to OH, then the demand

for money to hold in cash increases to ON.

(ii) Supply of Money:

The supply of money depends upon the currency issued by the central bank or

the policy followed by the government of the country. The supply of money

consists of currency and demand deposits. In the short run, the supply of money

is assumed to be constant.

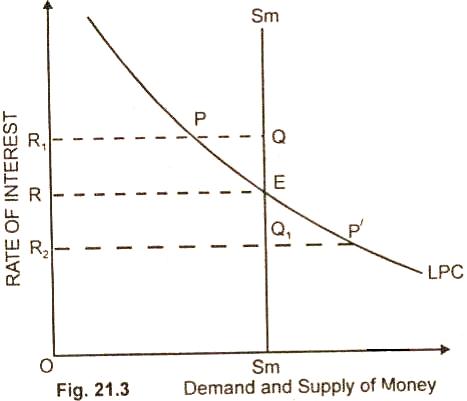

Determination of the rate of interest.

According to J.M. Keynes:

The rate of interest is determined at a where

demand for money is equal to the supply of money.

M = Sm

M = Total demand for money.

Sm = supply of money.

In the figure (21.3), the rate of interest as determined by the interaction

of the forces of demand and supply of money is OR, if there is any deviation

from this interest rate, it will not be stable. For example, if the interest

rate is OR1 it will lead to more supply of money (by PQ) than its demand. This

will lead to fall in the interest rate. The interest rate OR2 is also not

stable. Here demand for money is more than its supply by P/Q1. This will lead to

rise in interest rate.

Criticism:

Keynes theory of interest is

criticized on the following grounds:

(i) Indeterminate: J M. Keynes has criticized the classical theory of

interest as being indeterminate. According to him, these theories do not take

income changes into account. The fact is that Keynes theory of interest itself

assumes a particular level of income and does not take income changes into

account. As such it is also indeterminate.

(ii) Ignores real factors: The theory put forward by Keynes offers only a

monetary explanation of the determination of rate of interest. It altogether

ignores the real factors such as marginal productivity of capital, thrift etc.,

which work behind the demand for money and supply of it.

(iii) No liquidity without saving: According to Keynes, interest is the reward

for parting with liquidity. It is in no way as inducement for saving. According

to Jocob Viner, it is saving which makes funds available to be kept as liquid.

Without saving, there can be no liquidity to surrender. Keynes has ignored this

aspect in the determination of rate of interest.

(iv) Interest in the short run: Keynes theory explain the determination of the

rate of interest in the short run. It fails to explain the rate of interest in

the long run.

(v) Not an integrated theory: According to Hicks, Learner, the rate of

interest along with the level of income is determined by (a), marginal

efficiency of capital, (b) consumption function, (c) the liquidity preference function and (d) the quantity of money function. Keynes has discussed the

last two elements in his interest theory and has ignored the. first two

elements. The theory of interest is, thus, not properly integrated by Keynes.

(6) Modern Theory of

Interest/IS-LM Curve Model:

Definition:

The Modern Theory of Interest is designated as

IS-LM Curves Model.

Hicks-Hansen's, IS-IM curves model seeks to explain a case of joint determination

of equilibrium rate of interest (r) and equilibrium level of income (y).

This theory is designed to explain the joint determination of equilibrium

rate of interest r and equilibrium level of income y by the interaction

of the commodity market and money market. Since IS curve and LM curve indicate

equilibrium in the commodity market and equilibrium in the money market

respectively, so the intersection of IS curve and LM curve shows the

simultaneous equilibrium in both the commodity market and money market with

equilibrium rate of interest r and equilibrium level of national income y.

(i) Equilibrium in the

Commodity Market (Real Sector), Derivation of IS curve/Diagram:

The equilibrium in the commodity market can be determined on the basis of

following postulates:

Assumptions/Postulates:

(i) Level of Saving S is an increasing function of both the rate of interest r

and level of income y. It implies that as the rate of interest r rises,

savings S also rises. Likewise, as the level of income Y rises, saving S also

rises. Symbolically:

Formula:

S = f (r,y), ∂s > 0 ∂s > 0

∂r ∂y

(ii) Level of investment I is a decreasing function of the rate of interest, it

implies that as the rate of interest r falls, the level of investment I

rises. However, as the level of income Y rises, the level of investment I also

rises. Symbolically:

I = f (r,y), ∂I < 0 ∂I > 0

∂r ∂y

The commodity market will be in equilibrium when savings = investment, that

is:

S = I

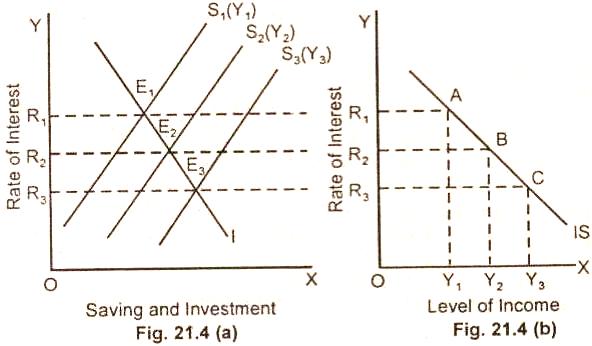

We show the derivation of IS curve

by determining equilibrium in the

commodity market in terms of equilibrium between savings S and investment I

corresponding to different pairs of interest rate rand the level of income Y.

Fig. 21.4(a) depicts that at level of income Y1 and rate of interest

R1,

saving S is equal to investment I at E1 signifying equilibrium in the commodity,

market. The corresponding point to E1 is A representing S = l in fig.

21.4(b).

At

level of income Y2 and rate of interest R2, saving S is equal to investment I at E2 denoting equilibrium in the commodity market. The corresponding point

to E2 is B representing S = I.

Likewise, at level of income Y3

and rate of interest R3, saving is equal investment at E3 indicating equilibrium in the

Commodity, market. The corresponding point to E3 is C representing S = I. In

Fig. 21.4(b), by joining points A, B and C, we obtain IS curve.

Definition of IS

Curve:

"Thus

IS curve is that curve which shows equilibrium in the commodity market

corresponding to different pairs of level of income Y and rate of

interest r".

The IS curve slopes downward from left to right indicating the

inverse relation between the rate of interest and the level of income. It is

because of the fact that when rate of interest falls, the level of investment

rises leading to rise in the level, of income.

(ii) Equilibrium in the Money Market (Monetary Section), Derivation of

LM Curve:

The equilibrium in the money market can be determined

on the basis of following postulates:

Assumptions/Postulates:

(i) The demand for money L is an

increasing function of level of income Y. It means that when the level of income

Y rises, the demand for money L also rises. However, the demand for money L is a

decreasing function of the rate of interest r. It implies that when the rate of

interest r falls, the demand for money L rises. Symbolically:

L = f (r,y), ∂L > 0 ∂L < 0

∂r ∂y

(ii) The supply of money M is assumed fixed as it is exogenously determined. The

money market will be in equilibrium when demand for money = supply of

money, that is:

L = M

Diagram of LM

Curve:

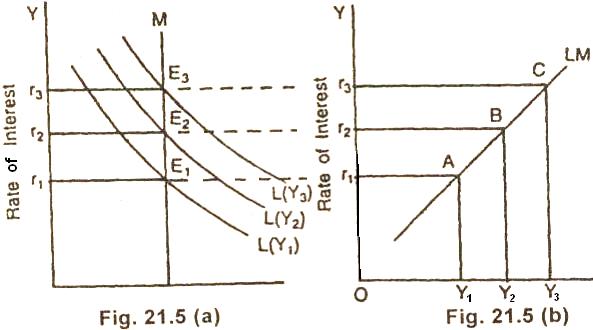

We drive LM curve by determining equilibrium in the money market in terms of

equilibrium between demand for money L and supply of money M corresponding to

different pairs of interest rate r and the level of income Y. Fig, 21.5(a) shows

that at level of income Y1 and rate of interest r1 demand for money L and supply

of money M equilibrate at E1 signifying equilibrium in the money market. The

corresponding point to E1 is A representing L = M in Fig. 21.5(b).

At level of

the income Y2

and rate of interest r2, demand for money L and supply of money M are

equal at E2 denoting equilibrium in the money market. The

corresponding point to E2 is B representing L = M likewise at level

of income Y3 and rate of interest r3, demand for money

Land supply of money M are equal at E3 indicating equilibrium in

money market. The corresponding point to E3 is C representing L = M.

In Fig. 21.5(b), by joining points A,

B and C we obtain LM curve. Thus, LM curve is that curve which shows equilibrium

in the money market corresponding to different pairs of level of income Y and

rate of interest r. The LM curve slopes upward from left to right indicating

direct relation between level of income and the rate of interest It is due to

the fact that given the stock of money supply, as the level of income rises the

transaction demand for money rises pushing tap the rate of interest.

Simultaneous Equilibrium in the Commodity Market and Money Market:

After having derived IS curve and LM curve, we how make use of

IS-LM curves

to demonstrate simultaneous determination of both the equilibrium rate of

interest and the equilibrium level of-national income.

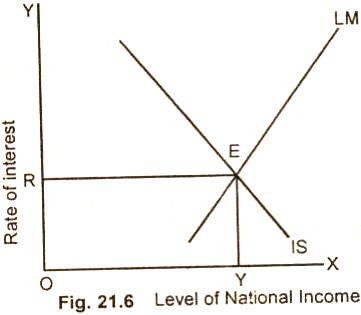

In Fig. 21.6, IS curve

and LM curve interest at E to determine the equilibrium rate of interest Or and

the equilibrium level of national income OY. It is imperative to point out that

it is only at Or rate of interest and OY level national income that saving is

equal to investment and demand for money is equal to supply of money. If implies

that it is only at rate of interest Or and level of national income OY

that the economy is in equilibrium involving simultaneous equilibrium of both

the real sector (commodity market) and the monetary sector (money market).