Degrees of Elasticity of

Demand:

We have

stated demand for a product is sensitive or responsive to price change. The

variation in demand is, however, not uniform with a change in price. In case of

some products, a small change in price leads to a relatively larger change in

quantity demanded.

Elastic and Inelastic Demand:

For example,

a decline of 1% in price leads to 8% increase in the quantity demanded of a

commodity. In such a case, the demand is said to elastic. There

are other products where the quantity demanded is relatively unresponsive to

price changes. A decline of 8% in price, for example, gives rise to 1% increase

in quantity demanded. Demand here is said to be inelastic.

The terms

elastic and inelastic demand do not indicate the degree of responsiveness and

unresponsiveness of the quantity demanded to a change in price.

The

economists therefore, group various degrees of elasticity of demand into

five categories.

(1)

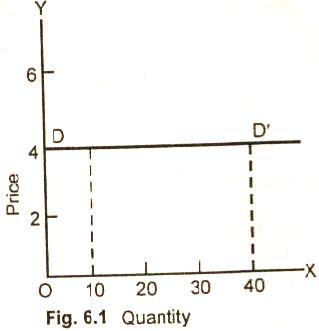

Perfectly Elastic Demand:

A demand is perfectly elastic when a small

increase in the price of a good its quantity to zero. Perfect elasticity implies

that individual producers can sell all they want at a ruling price but cannot

charge a higher price. If any producer tries to charge even one penny more, no

one would buy his product.

People would prefer to buy from another producer who

sells the good at the prevailing market price of $4 per unit. A perfect elastic

demand curve is illustrated in fig. 6.1.

Diagram:

It shows that the demand curve DD/

is a horizontal line which indicates that the quantity demanded is extremely

(infinitely) response to price. Even a slight rise in price (say $4.02), drops

the quantity demanded of a good to zero. The curve DD/ is infinitely

elastic. This elasticity of demand as such is equal to infinity.

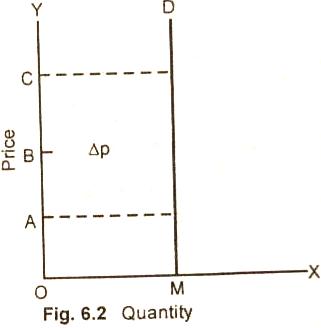

(2)

Perfectly Inelastic Demand:

When the

quantity demanded of a good dose not change at all to whatever change in price,

the demand is said to be perfectly inelastic or the elasticity of demand is

zero.

For example,

a 30% rise or fall in price leads to no change in the quantity demanded of a

good.

Ed = 0

30%

Ed = 0

In figure 6.2

a rise in price from OA to OC or fall in price from OC to OA causes no change

(zero responsiveness) in the amount demanded.

Ed = 0

Δp

Ed = 0

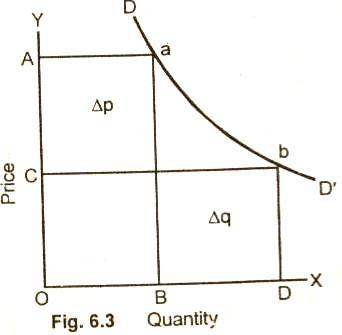

(3)

Unitary Elasticity of Demand:

When the quantity demanded of a good changes

by exactly the same percentage as price, the demand is said to has a unitary

elasticity.

For example, a 30% change in price leads to 30% change quantity

demand = 30% / 30% = 1.

One or a one

percent change in price causes a response of exactly a one percent change in the

quantity demand.

In this figure (6.3) DD/ demand curve with unitary

elasticity shows that as the price falls from OA to OC, the quantity demanded

increases from OB to OD. On DD/ demand curve, the percentage change

in price brings about an exactly equal percentage in quantity at all points a,

b. The demand curve of elasticity is, therefore, a rectangular hyperbola.

Ed = %∆q

%∆p

Ed = 1

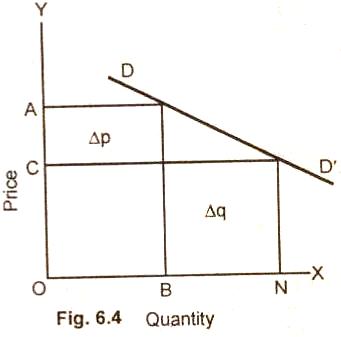

(4)

Elastic Demand:

If a one

percent change in price causes greater than a one percent change in quantity

demanded of a good, the demand is said to be elastic.

Alternatively, we can say that the elasticity of demand is greater than. For

example, if price of a good change by 10% and it brings a 20% change in demand,

the price elasticity is greater than one.

Ed = 20%

10%

Ed = 2

In figure

(6.4) DD/ curve is relatively elastic along its entire length. As the

price falls from OA to OC, the demand of the good extends from OB to ON i.e.,

the increase in quantity demanded is more than proportionate to the fall in

price.

Ed = %∆q

%∆p

Ed > 1

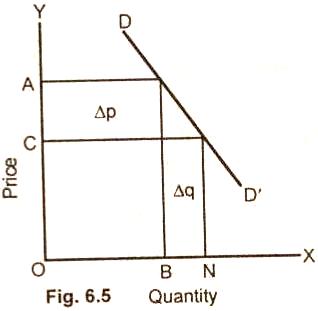

(5) Inelastic Demand:

When a change

in price causes a less than a proportionate change in quantity demand, demand is

said to be inelastic.

The

elasticity of a good is here less than I or less than unity. For example, a 30%

change in price leads to 10% change in quantity demanded of a good, then:

Ed = 10%

30%

Ed = 1

3

Ed < 1

In figure

(6.5) DD/ demand curve is relatively inelastic. As the price fall

from OA to OC, the quantity demanded of the good increases from OB to ON units.

The increase in the quantity demanded is here less than proportionate to the

fall in price.

Note:

It may here note that the slope of a demand curve is not a reliable indicator of

elasticity. A flat slope of a demand curve must not mean elastic demand.

Similarly, a steep slope on demand curve must not necessarily mean inelastic

demand.

The reason is

that the slope is expressed in terms of units of the problem. If we change the

units of problem, we can get a different slope of the demand curve. The

elasticity, on the other hand, is the percentage change in quantity demanded to

the corresponding percentage change in price.

Relevant Articles:

|