Effects of Changes in

Demand on Equilibrium Market:

We

know that if the price rises, other things remaining the same, people buy

less of that commodity and if price falls, people buy more of that commodity.

Let us now discuss the effects of changes in demand on

equilibrium price.

A change to

demand can take place independently of change in price, i.e., price remaining

the same, people may purchase more or less of the commodity. When larger

quantity is demanded at the same old price or the same old quantity is demanded

at a higher price we say, the demand has risen. In such a case, the whole of

demand curve rises above the original demand curve. In case of a fall in demand,

the whole of the demand curve falls below the original demand curve.

In order to

study the effect of the changes in demand on equilibrium price, let us assume

that no change takes place in the supply schedule, i.e., it remains fixed. If

demand rises, more quantity will be purchased at a higher price. On the other

hand, if demand falls, less commodity will be purchased at a lower price. This

can also be illustrated in the following diagram.

Diagram/Figure:

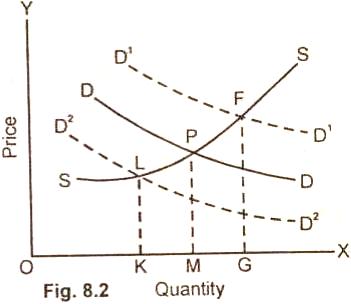

In the

figure (8.2) DD/ is the original demand curve. PM is the equilibrium price and OM the

equilibrium amount. When demand rises, supply remaining the same, the

equilibrium amount increases from OM to OG and the equilibrium price rises from

PM to FG. In case of fall of in demand, which is indicated by D2D2

curve, the quantity demanded decreases from OM to OK and the equilibrium price

falls from PM to LK.

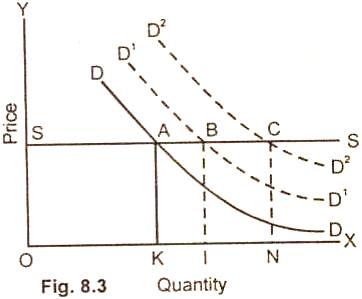

Now a

question can be asked that when the demand rises, does it affect more on the

price or on the quantity of the commodity to be sold? The answer to this simple

question, is that if the supply is perfectly elastic, a rise in demand will

increase the quantity but will not affect the price. If the supply is perfectly

inelastic, then a rise in demand will affect the price but not the quantity.

This can be shown with the help of the diagram. In case of perfect elastic

supply, (Fig. 8.3) when demand rises, the supply increases from OK to OI with

further rise in demand D2D2 the supply increases from OI

to ON.

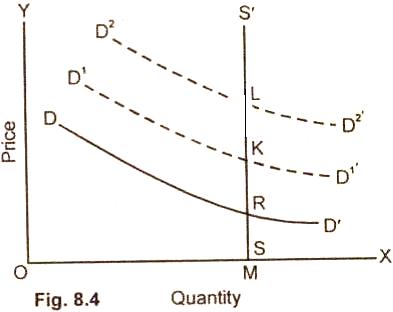

Supply

Perfectly Inelastic:

In fig. 8.4,

the supply is perfectly inelastic. A rise in demand affects the price which

rises from RM to KM and with the further rise in demand to LM. The quantity

supplied remains the same OM.

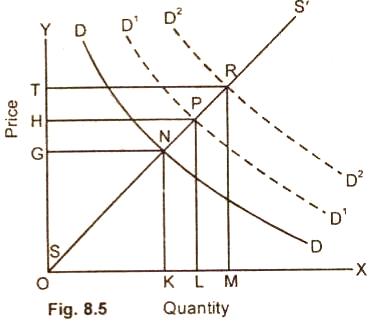

In the the

world in which we live, the supply is seldom perfectly elastic or perfectly

inelastic. It is either equal to unity or greater than unity, or less than

unity. We will, therefore, examine these, cases now. If elasticity of supply is

to unity and demand rises, the price and quantity will change in equal

proportion.

(i)

Elasticity of Supply is Equal to Unity:

The quantity and price change in

equal proportion with a rise in demand as is clear in fig. 8.5.

(ii)

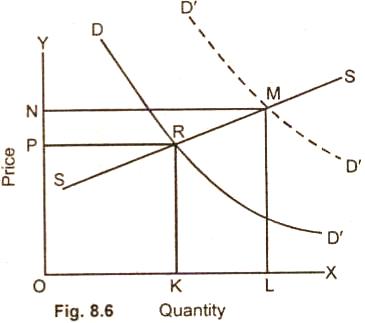

Elasticity of Supply Greater Than Unity:

If the

elasticity of supply is greater than unity, a

rise in demand will affect the supply which will change in greater proportion

than the price as is obvious from the following fig. 8.6.

In fig. (8.6)

when demand rises, KL quantity supplied is greater in proportion than PN price.

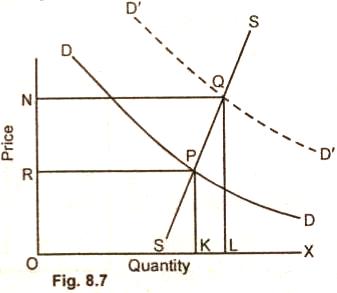

(iii) Elasticity of Supply

Less Than Unity:

If the elasticity of supply is less

than unity, a rise in demand will change the price in greater proportion than

the quantity as shown in fig. 8.7.

In fig. 8.7 the proportionate

change in quantity demanded KL is less than the change in price

RN.

Relevant Articles:

|