Long Run Equilibrium Under Monopoly:

The

monopolist creates

barriers of entry for the new firms into the industry. The

entry into the industry is blocked by having control over the raw materials

needed for the production of goods or he may hold full rights to the production

of a certain good (patent) or the market of the good may be limited. If new

firms try to enter in the field, it lowers the price of the good to such on

extent that it becomes unprofitable for new firms to continue production etc.

When

there is no threat of the entry of new firms into the industry, the monopoly

firm makes long run adjustments in the scale of plant. In case, the demand for

the product is limited, the monopolist can afford to produce output at sub

optimum scale. If the market size is large and permits to expand output, then

the monopolist would build an optimum scale of plant and would produce goods at

the minimum cost per unit. However, the monopolist would not stay in the

business, if he makes losses in the long period. The long run equilibrium of a

monopoly firm is now explained with the help of the following diagram.

Diagram/Curve:

In the

long run, all the factors of production including the size of the plant are

variable. A monopoly firm will maximize profit at that level of output for which

long run marginal cost (MC) is equal to marginal revenue (MR) and the LMC curve

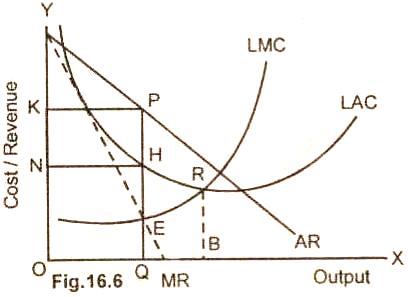

intersects the MR curve from below. In the figure (16.6), the monopoly firm is

in equilibrium at point E where LMC = MR and LMC cuts MR curve from below. QP is

the equilibrium price and OQ is the equilibrium output.

At OQ level of output,

the cost per unit is QH (LAC), whereas the price per unit of the good is QP. HP

represents the per unit super normal profit. The total super normal profit is

equal to KPHN. It may here be noted that at the equilibrium output OQ, the plant

is not being fully utilized. The long run average cost (LAC) is not minimum at

this level of output OQ. The firm will build an optimum scale of plant only if

the demand for the product increases.

Threat of Entry of New Firms:

If there is a threat of

entry of new firms into the market,

the monopolist adopts price reduction strategy. He instead of charging QP price

per unit, lowers the price to BR. Since the per unit price BR is equal to the

cost per unit at R, the monopoly firm is earning only normal profit in the long

run. The reduction in price and so in profits is adopted to prevent the entry of

new firms in the market.

Summing up, if a monopoly firm is in a position

to maintain its monopoly status, it can earn super normal profit in the long

period. However, if there is an effective threat of the entry of potential firms

in, the industry, then the firm can earn just normal profit by reducing the

price. The reduction in price depends on how strong is the threat of potential

entry into the industry.

Relevant Articles:

|