The modern economists like Pareto, Mrs. Joan Robinson, Boulding, Sligler,

Shepherd, have tried to simplify and generalize the

ricardian theory of rent.

According to them, the Ricardian theory of rent is too closely related to land.

This creates on impression that rent is a peculiar earning of land only. The

fact, however, is that other factors of production i.e., labor, capital and

entrepreneurship may also be earning economic rent. The determination of rent,

the modem economists say, can be explained in the same manner as the reward of

other factors, that is by demand and supply forces.

Demand and Supply Analysis:

(A) Demand For a

Factor:

The demand for a factor which may be land,

labor or

capital is a derived demand. Land, say for instance, is demanded for its

produce. The higher the produce, the greater is the demand for land. A firm

will pay rent equal to the marginal revenue productively of land. The rent

diminishes as more land is used due to the operation of

law of diminishing

returns. The demand curve of a factor is, therefore, negatively sloped which

means more land will be used only at lower rents, other things of course

remaining the same.

Supply of a factor.

The supply of land to a particular use (say industry) is quite elastic. It

can be shifted to other uses by offering higher rent than that being earned by

it now. The supply of a factor (to an industry) is, therefore, rent elastic. If

higher rent is paid, the supply of a factor can be increased by withdrawing it

from other uses. The supply curve of a factor (industry) slopes upward to the

right.

Diagram:

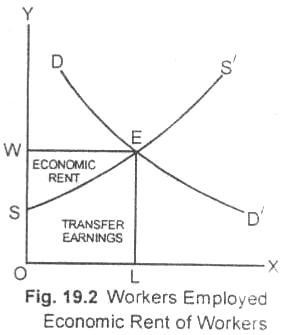

Determination of rent.

The economic rent is determined by the intersection of demand and supply

curves for a factor. In this figure (19.2), the demand curve for a factor say

labor in a particular industry is DD/ and the supply curve of workers is SS/.

The wage rate or factor price of labor as determined by the market forces is

OW. The total workers employed in a particular industry at OW wage rate is OL.

The total earning of the workers employed is equal to the area OWEL. At wage rate

OW, there are workers who would work, at lower pay but they are also paid at

OW

wage rate. Those workers whose transfer earnings are less than this wage

rate will be getting economic rent. The total economic rent earned by all the intra marginal workers is equal in

the area WES. The marginal worker i.e., Lth worker is not obtaining any rent or

surplus.

(B) Rent is a Surplus

Return:

The modern economists are also of the view that

rent as a surplus can be earned by other factors also. It is not peculiar to

land alone as explained by Ricardo. The modern theory of rent is that it is the

difference between the actual earning of a factor unit over its transfer

earnings. The transfer earnings of a factor of production is the minimum payment

required for preventing that factor for transferring it to some other use. It is

called the factor supply price in its present occupation.

For example, a worker

earns $6000 per month in a factory. In the next best employment, he can get $5000 only per month. The surplus or excess of

$1000 which a worker is

earning over and above the minimum payment necessary for inducting him to work

in the present occupation is the economic rent.

Economic Rent Depends on the

Elasticity of Supply of the Factor of Production:

The proportion of the income of a factor that consists of economic

rent depends on the elasticity of supply of the factor of production which may

be (i) totally inelastic supply (ii) perfectly elastic supply and (iii) less than

perfectly elastic supply.

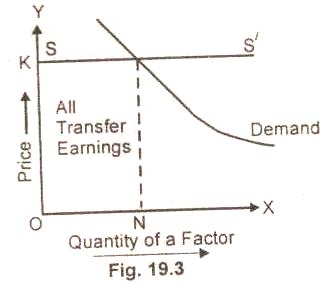

(i) Perfectly elastic supply.

When the supply of a factor of production is perfectly elastic, then none of its

income is economic rent. Its entire income is transfer earnings.

In the Fig. 19.3, the supply curve SS/ is a horizontal line. Whatever the

amount of factor demanded, the supply price remains at OS. Hence, it

earns no surplus in the nature of rent.

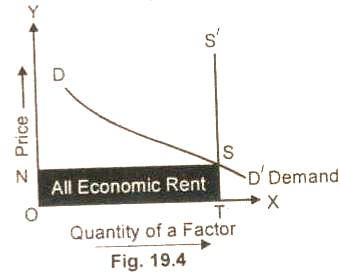

(ii) Totally inelastic supply. When the supply of a factor is

totally inelastic, then its transfer earnings is zero. The entire income is

economic rent.

In the fig. 19.4, the elasticity of the supply of factor of

production is zero. It does not increase at all as its demand increases. The

supply curve is vertical. The entire of factor income is a surplus which is shown by

area ONST.

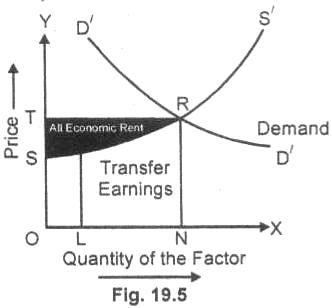

(iii) Less than perfectly elastic supply. If the supply of a factor of production is neither perfectly elastic nor perfectly inelastic as

illustrated