Law of Diminishing Returns/Law

of Increasing Cost:

(Version of Classical and Neo

Classical Economists):

Definition:

The law of diminishing returns

(also called the Law of Increasing Costs) is an important

law of micro economics. The law of diminishing returns

states that:

"If an increasing amounts of a variable factor are

applied to a fixed quantity of other factors per unit of time,

the increments in total output will first increase but beyond

some point, it begins to decline".

Richard A. Bilas describes the

law of diminishing returns in the following words:

"If the input

of one resource to other resources are held constant, total

product (output) will increase but beyond some point, the

resulting output increases will become smaller and smaller".

The

law of diminishing return can be studied from two points of

view, (i) as it applies to agriculture and (ii) as it

applies in the field of industry.

(1)

Operation of Law of Diminishing Returns in Agriculture:

Traditional Point of View.

The classical economists were of the opinion that the taw of

diminishing returns applies only to agriculture and to some

extractive industries, such as mining, fisheries urban land,

etc. The law was first stated by a Scottish farmer as such. It

is the practical experience of every farmer that if he wishes to

raise a large quantity of food or other raw material

requirements of the world from a particular piece of land, he

cannot do so. He knows it fully that the producing capacity of

the soil is limited and is subject to exhaustation.

As he

applies more and more units of labor to a given piece of land,

the total produce no doubt increases but it increases at a

diminishing rate.

For example, if the number of

labor is doubled, the total yield of his land will not be

double. It will be less than double. If it becomes possible to

increase the. yield in the very same ratio in which the units of

labor are increased, then the raw material requirements of

the whole world can be met by intensive cultivation in a single

flower-pot. As this is not possible, so a rational farmer

increases the application of the units of labor on a piece of

land up to a point which is most profitable to him. This is in

brief, is the law of diminishing returns. Marshall has

stated this law as such:

"As Increase in capital and labor

applied to the cultivation of land causes in general a less than

proportionate increase in the amount of the produce raised,

unless it happens to coincide with the improvement in the act of

agriculture".

Explanation

and Example:

This law can be made more clear if

we explain it with the help, of a schedule and a curve.

Schedule:

|

Fixed Input |

Inputs of Variable Resources |

Total Produce TP (in tons) |

Marginal product MP (in

tons) |

|

12 Acres

12 Acres

12 Acers

12 Acres

12 Acers

12 Acres |

1 Labor

2 Labor

3 Labor

4 Labor

5 Labor

6 Labor |

50

120

180

200

200

195 |

50

70

60

20

0

-5 |

In the schedule given above, a firm

first cultivates 12 acres of land (Fixed input) by applying one

unit of labor and produces 50 tons of wheat.. When it applies 2

units of labor, the total produce increases to 120 tons of

wheat, here, the total output increased to more than double by

doubling the units of labor. It is because the piece of land is

under-cultivated. Had he applied two units of labor in the very

beginning, the marginal return would have diminished by the

application of second unit of labor.

In our schedules the rate

of return is at its maximum when two units of labor are applied.

When a third unit of labor is employed, the marginal return

comes down to 60 tons of wheat With the application of 4th

unit. the marginal return goes down to 20 tons of wheat and when

5th unit is applied it makes no addition to the total

output. The sixth unit decreased it. This tendency of marginal

returns to diminish as successive units of a variable resource

(labor) are added to a fixed resource (land), is called the law

of diminishing returns. The above schedule can be represented

graphically as follows:

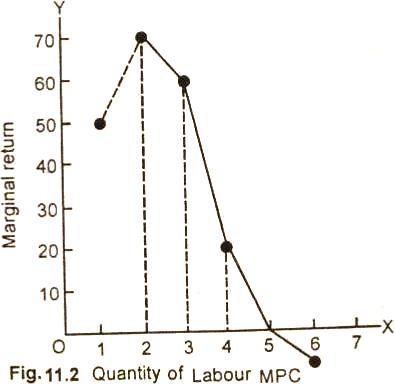

Diagram/Graph:

In Fig. (11.2) along OX are measured doses of labor applied to a

piece of land and along OY, the marginal return. In the

beginning the land was not adequately cultivated, so the

additional product of the second unit increased more than of

first. When 2 units of labor were applied, the total yield was

the highest and so was the marginal return. When the number of

workers is increased from 2 to 3 and more. the MP begins to

decrease. As fifth unit of labor was applied, the marginal

return fell down to zero and then it decreased to 5 tons.

Assumptions:

The table and the diagram is based

on the following assumptions:

(i) The time is too short for a firm

to change the quantity of fixed factors.

(ii) It is assumed that labor is the

only variable factor. As output increases, there occurs no

change in the factor prices.

(iii) All the units of the variable

factor are equally efficient.

(iv) There are no changes in the

techniques of production.

(2)

Operation of the Law in the Field of Industry:

The modern economists are of the

opinion that the law of diminishing returns is not exclusively

confined to agricultural sector, but it has a much wider application.

They are of the view that whenever the supply of any essential

factor of production cannot be increased or substituted

proportionately with the other sectors, the return per unit of

variable factor begins to decline. The law of diminishing

returns is therefore, also called the Law of Variable

Proportions.

In agriculture, the law of diminishing returns

sets in at an early stage because one very important factor,

i.e., land is a constant factor there and it cannot be increased

in right proportion with other variable factors, i.e., labor and

capital. In industries, the various factors of production can be

co-operated, up to a certain point. So the additional return per

unit of labor and capital applied goes on increasing till there

takes place a dearth of necessary agents of production. From

this, we conclude that the law of diminishing return arises from

disproportionate or defective combination of the various agents

of production. Or we can any that when increasing amounts of a

variable factor are applied to fixed quantities of other

factors, the output per unit of the variable factor eventually

decreases.

Mrs. John Robinson goes deeper into

the causes of diminishing returns and says that:

"If all factors

of production become perfect substitute for one another, then

the law of diminishing returns will not operate at any stage".

For instance, if sugarcane

runs short of demand and some other raw material takes its place

as its perfect substitute, then the elasticity of substitution

between sugarcane and the other raw material will be infinite.

The price of sugarcane will not rise and so the law of

diminishing returns will not operate.

The law of diminishing returns,

therefore, in due to Imperfect substitutability of factors of

production.

The law of diminishing returns is

also called as the Law of Increasing Cost. This is because of

the fact that as one applies successive units of a variable

factor to fixed factor, the marginal returns begin to diminish.

With the cost of each variable factor remaining unchanged by

assumptions and the marginal returns registering .decline, the

cost per unit in general goes on increasing. This tendency of

the cost per unit to rise as successive units of a variable

factor are added to a given quantity of a fixed factor is called

the law of Increasing Cost.

Importance:

The law of diminishing returns

occupies an important place in economic theory. The British

classical economists particularly Malthus, and Ricardo

propounded various economic theories, on its basis. Malthus, the

pessimist economist, has based his famous theory of Population

on this law.

The Ricardian theory of rent is also based on the

law of diminishing return. The classical economists considered

the law as the inexorable law of nature.

Relevant Articles:

|