Average Cost:

Definition and Explanation:

The entrepreneurs are no doubt

interested in the total costs but they are equally concerned in

knowing the cost per unit of the product. The unit cost figures

can be derived from the

total fixed cost, total variable cost and total cost by

dividing each of them with corresponding output.

Types/Classifications:

(1) Average

Fixed Cost (AFC):

Average fixed cost refers to fixed

cost per unit of output. Average fixed Cost is found out by

dividing the total fixed cost by the corresponding output.

Formula:

AFC = TFC

Output

(Q)

For instance, if the total

fixed cost of a shoes factory is $5,000 and it produces 500

pairs of shoes, then the average fixed cost is equal to $10 per

unit. If it produces 1,000 pairs of shoes, the average fixed

cost is $5 and if the total output is 5,000 pairs of shoes, then

the average fixed cost is $1 pair of shoe.

From the above example, it is clear,

that the fixed cost, i.e., $5,000 remains the same whether the

output is 1,000 or 5,000 units.

Behavior of Average Fixed

Cost (AFC):

The average fixed cost begins to

fall with the increase in the number of units produced, In our

example stated above, average fixed cost in the beginning was

$10. As the output of the firm increased, it gradually came down

to $1. The AFC diminishes with every increase in the quantity of

output produced but it never becomes zero.

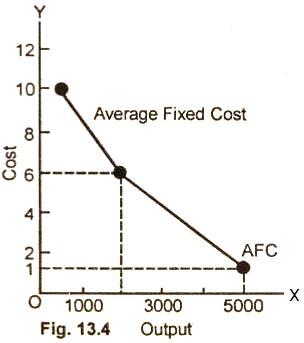

Diagram/Curve:

The concept of average fixed cost

can be explained with the help of the curve, in the diagram

(13.4) the average fixed cost curve gradually falls from left to

right showing the level of output. The larger the level of

output, the lower is the average fixed cost and smaller the

level of output, the greater is the average fixed cost. The AFC

never becomes zero.

(2) Average

Variable Cost (AVC):

Average variable cost

refers to the variable expenses per unit of output Average

variable cost is obtained by dividing the total variable cost by

the total output.

For instance, the total

variable cost for producing 100 meters of cloth is $800, the

average variable cost will be $8 per meter.

Formula:

AVC = TVC

(Q)

Behavior of Average Variable

Cost:

When a firm increases its output, the average variable

cost decreases in the beginning, reaches a minimum and then

increases. Here, a question can be asked as to why AVC decreases

in the beginning reaches a minimum and then increases. The

answer to this question is very simple.

When in the beginning, a

firm is not producing to its full capacity, then the various

factors of production employed for the manufacture of a

particular commodity remain partially absorbed. As the output of

the firm is increased, they are used to its fullest extent. So

the AVC begins to decrease. When the plant works to its full

capacity, the AVC is at its minimum. If the production is pushed

further from the plant capacity, then less efficient machinery

and less, efficient labour may have to be employed. This results

in the rise of AVC. It is in this way we say that as the output

of a firm increases, the AVC decreases in the beginning, reaches

a minimum and then increases. The AVC can also be represented in

the form of a curve.

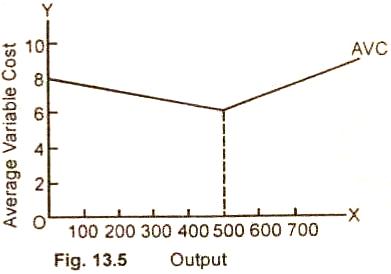

Diagram/Curve:

The shape of the average variable

cost curve (Fig. 13.5) is like a flat U-shaped curve. It shows

that when the output is increased, there is a steady fall in the

average variable cost due to increasing returns to variable

factor. It is minimum when 500 meters of doth are produced. When production is

increased to 600 meters, of cloth or more, the average variable

cost begins to increase due to diminishing returns to the

variable factor.

(3) Average

Total Cost (ATC):

Average total cost refers to cost

(both fixed and variable) per unit of output. Average total cost

is obtained by dividing the total cost by the total number of

commodities produced by the firm or when the total sum of

average variable cost and average fixed cost is added together,

it becomes equal to average total cost.

Formula:

ATC = Total Cost (TC)

Output

(Q)

Behavior of Average Total

Cost:

As the output of a firm increases, average total cost

like the average variable cost decreases in the beginning

reaches a minimum and then it increases. The reasons for decline

of ATC in the beginning are that it is the sum of AFC and AVC.

Average fixed cost and average

variable costs have both the tendency to fall as output is

increased. Average total cost will continue falling so long

average variable cost does not rise. Even if average variable

cost continues rising, it is not necessary that the average

total cost will rise. It can be due to the fact that the

increase in average variable cost is less than the fall in

average fixed cost. The increase in average variable cost is

counterbalanced by a rapid fall of average fixed cost. If the

rise in the average variable cost is greater than the fall in

average fixed cost, then the average total cost will rise.

The tendency to rise on the part of

average total cost-in the beginning is slow, after a certain

point it begins to increase rapidly.

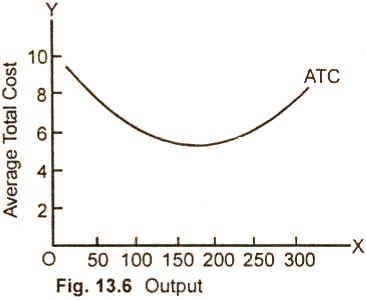

Diagram/Curve:

The average total cost is

represented here by a shaped curve in Fig. (13.6). The average total cost curve is also

like a U-shaped curve. It shows that as production increases

from 100 meters to 200 meters of cloth, the cost falls rapidly,

reaches a minimum but then with higher level of output, the

average fixed cost begins to increase.

Relevant Articles:

|