Marginal Cost

(MC):

Definition:

Marginal Cost is an increase

in total cost that results from a one unit increase in output.

It is defined as:

"The cost that results from a one unit change

in the production rate".

Example:

For example, the total cost of

producing one pen is $5 and the total cost of producing two pens

is $9, then the marginal cost of expanding output by one unit is

$4 only (9 - 5 = 4).

The marginal cost of the second unit

is the difference between the total cost of the second unit and

total cost of the first unit. The marginal cost of the 5th unit

is $5. It is the difference between the total cost of the 6th

unit and the total cost of the, 5th unit and so forth.

Marginal Cost is governed only by

variable cost which changes with changes in output. Marginal

cost which is really an incremental cost can be expressed in

symbols.

Formula:

Marginal Cost = Change in Total

Cost = ΔTC

Change

in Output Δq

The readers can easily understand

from the table given below as to how the marginal cost is

computed:

Schedule:

|

Units of Output

|

Total Cost

(Dollars) |

Marginal Cost (Dollars) |

|

1 |

5 |

5 |

|

2 |

9 |

4 |

|

3 |

12 |

3 |

|

4 |

16 |

4 |

|

5 |

21 |

5 |

|

6 |

29 |

8 |

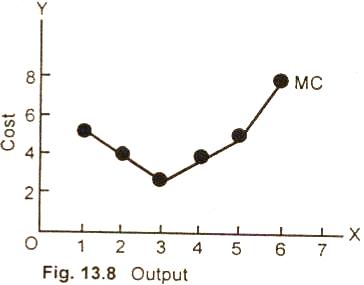

Graph/Diagram:

MC curve,

can also be plotted graphically. The marginal cost curve in

fig. (13.8) decreases sharply with smaller Q output and reaches

a minimum. As production is expanded to a higher level, it

begins to rise at a rapid rate.

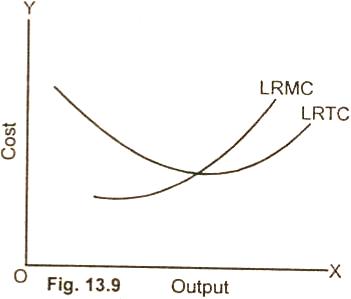

Long Run Marginal Cost Curve:

The long run marginal cost curve like the long run average cost

curve is U-shaped. As production expands, the marginal cost

falls sharply in the beginning, reaches a minimum and then rises

sharply.

Relationship Between Log Run

Average Cost and Marginal Cost:

The relationship between the

long run average total cost and log run marginal cost can be

understood better with the help of following diagram:

It is clear from the diagram (13.9),

that the long run marginal cost curve and the long run average

total cost curve show the same behavior as the short run

marginal cost curve express with the short run average total

cost curve. So long as the average cost curve is falling with

the increase in output, the marginal cost curve lies below the

average cost curve.

When average total cost curve begins to

rise, marginal cost curve also rises, passes through the minimum

point of the average cost and then rises. The only difference

between the short run and long run marginal cost and average

cost is that in the short run, the fall and rise of curves LRMC

is sharp. Whereas In the long run, the cost curves falls and

rises steadily.

Relevant Articles:

|