Equilibrium Price and Output in the Long Run

Under Monopolistic/Imperfect Competition:

Long

Run Zero Economic Profits:

In the long run, the

firms are able to alter the scale of plant according to the

changed conditions of demand for a product in the market. They

can also

leave or enter the

industry. If the firms are earning abnormal profits in the

short run, then new firm will enter the 'product group'

(industry). The tendency of the new firms to enter the industry

continues till the abnormal profits are competed away and the

firms economic profits are zero. In case the monopolistically

competitive firms realize losses in the short-run, then some of

the firms will leave the industry. The exit of the firm

continues till zero economic profits are restored with the

operating firms.

In the long-run,

there are no entry barriers for the new firms. The incoming

firms install latest machinery and try to differentiate their

products from those of the established firms. The old firms

operating with .the used machinery try to match up with the new

entrants by improved variety of products in their group. They

increase expenditure on advertisement and on other sales

promotional measures. They employ more qualified staff for.

making technical improvement in their products. Since all the

firms for their existence incur additional expenditure for

improving the quality of the products, the cost curves of all

the firms move up. Due to entry of new firms in the industry and

higher costs of production, the output of each competing firm is

reduced. There is, therefore, a waste in the economic resources

of the country. The equilibrium price and output in the long-run

is explained with the help of a diagram.

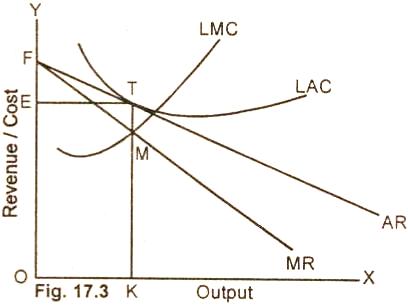

Diagram:

In the figure (17.3),

the higher shifted long-run marginal cost curve intersects the

higher shifted marginal revenue curve at point M. The firm at

this raised equilibrium point, produces the reduced level of

output OK. It sells this output at price TK as at point T, LAC

is a tangent to the demand or average revenue curve at its

minimum point. The total revenue of the firm is equal to the area OETK. The

total costs of the firm are also

equal to the area OETK. The firm is earning only zero or

normal economic profits. As the monopolistically competitive

firm sets a price higher than that minimum average cost in the

long-run, the firm therefore produces a smaller output. Since

all the firms in the product group produce less at higher price,

there is, therefore, an apparent waste of resources and

exploitation of the consumers.

The advocates of

monopolistic competition are of the opinion that if

consumers get differentiated products at slightly higher prices

(than with no choice under

perfect competition), the consumers are then not exploited.

There is no wasting of resources either, as the consumer's

welfare increases with the product differentiation.

Relevant Articles:

|