Monopolistic

competition refers to the market organization where there are a

fairly large number of firms which sell somewhat differentiated

products.

A single firm in the

product group (industry) has little impact on the market price.

However, if it reduces price, it can expect a considerable

increase in its sales. The firm may also attract buyers away

from other firms by creating imaginary or real difference

through advertising, branding and through many other sales

promotion measures (non-price

competition). If the firm raises its price, it will not lose

all its customers. This is because of the fact that the product

is differentiated from competing firms due to price and

non-price factors. The demand curve (AR curve) of the

monopolistic firm is therefore, highly elastic and is downward

sloping. As regards the marginal revenue curve, it slopes

downward and lies below the demand curve because price is

lowered of all the units to sell more output in the market.

Firm's Equilibrium Price and Output:

In the short-run, the

number of firms in the 'product

group' remains the same. The size of the plant of each firm

remains unaltered. The firm whether operating under perfect

competition, or monopoly wants to maximize profits. In order to

achieve this objective, it goes on producing a commodity so long

as the marginal revenue is greater than marginal cost. When MR =

MC, it is then in equilibrium and produces the best level of

output. If a firm produces less than or more than the MR = MC

output, it will then not be making maximum of profits.

In the short-run, a

monopolistically competitive firm may be realizing abnormal

profits or suffering losses. If it is earning profits, no new

firms can enter the industry in the short-run. In case, it is

suffering, losses but covering full variable cost, the firm will

continue operating so that the losses are minimized. If the full

variable cost is not met, the firm will close down in the

short-run. The short-run equilibrium with profits and short run

equilibrium with losses of a monopolistically competitive firm

are explained with the help of two separate diagrams as under.

Diagram:

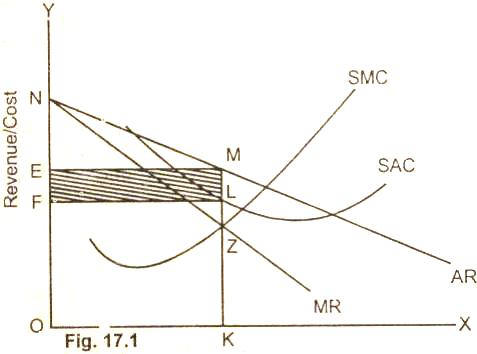

In the figure (17.1),

the downward sloping demand curve (AR curve) is quite elastic.

The MR curve lies below-the average curve except at point N. The

SMC curve which includes advertising and sales promotional costs

is drawn in the usual fashion. The SMC curve cuts the MR curve

from below at point Z. The firm produces and sells an output OK,

as at this level of output MR = MC. The firm sells output OK at

OE/KM per unit price. The total revenue of the firm is equal to

the area OEMK, whereas the total cost of producing output OK is

OFLK. The total profits of the firm are equal to the shaded

rectangle FEML. The firm earns abnormal profits in the short

run.

Short

Run Losses:

If the demand and

cost situations are not favorable in the market, a

monopolistically competitive firm may incur losses in the

short-run. The short-run equilibrium of the firm with losses is

explained with the help of a diagram.

Diagram:

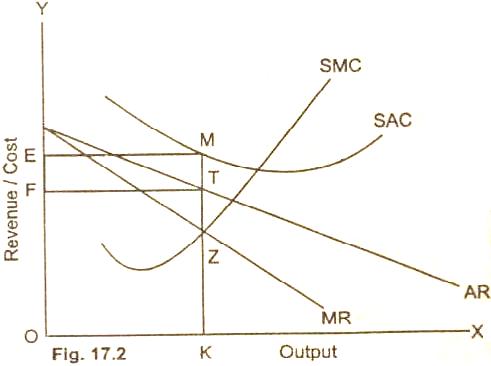

In the Figure (17.2),

marginal cost (SMC) equates marginal revenue MR curve from below

at point Z. The firm produces output OK and sells at OF/KT per

unit-price. The total receipt of the firm is OFTK. The total

cost of producing output OK is equal to OEMK. The firm suffers a

net loss equal to the area FEMT on the sale of OK output.