Optimum Factor Combination:

Definition:

In the

long run,

all factors of production can be varied. The profit maximization

firm will choose the least cost combination of factors to

produce at any given level of output. The least cost

combination or the optimum factor combination refers to the

combination of factors with which a firm can produce a specific

quantity of output at the lowest possible cost.

Explanation:

There are two methods of explaining

the optimum combination of factor:

(i) The marginal product approach.

(ii) The

isoquant / isocost approach.

These two approaches are now

explained in brief:

(i) The

Marginal Product Approach:

In the long run, a firm can vary the

amounts of factors which it uses for the production of goods. It

can choose what technique of production to use, what design of

factory to build, what type of machinery to buy. The profit

maximization will obviously want to use that mix of factors of

combination which is least costly to it. In search of higher

profits, a firm substitutes the factor whose gain is higher than

the other. When the last rupee spent on each factor brings equal

revenue, the profit of the firm is maximized. When a firm uses

different factors of production or least cost combination or the

optimum combination of factors is achieved when:

Formula:

Mppa = Mppb

= Mppc = Mppn

Pa

Pb Pc Pn

In the above equation a, b, c, n are

different factors of production. Mpp is the marginal physical

product. A firm compares the Mpp / P ratios with that of

another. A firm will reduce its cost by using more of those

factors with a high Mpp / P ratios and less of those with a low

Mpp / P ratio until they all become equal.

(ii) The

Isoquant / Isocost Approach:

The least cost combination

of-factors or producer's equilibrium is now explained with the

help of iso-product curves and isocosts. The optimum factors

combination or the least cost combination refers to the

combination of factors with which a firm can produce a specific

quantity of output at the lowest possible cost.

As we know,

there are a number of combinations of factors which can yield a

given level of output. The producer has to choose, one

combination out of these which yields a given level of output

with least possible outlay. The least cost combination of

factors for any level of output is that where the iso-product

curve is tangent to an isocost curve. The analysis of producers

equilibrium is based on the following assumptions.

Assumptions

of Optimum Factor Combination:

The main assumptions on which this

analysis is based areas under:

(a) There are two factors X and Y in

the combinations.

(b) All the units of factor X are

homogeneous and so is the case with units of factor Y.

(c) The prices of factors X and Y

are given and constants.

(d) The total money outlay is also

given.

(e) In the factor market, it is the

perfect completion which prevails. Under the conditions assumed

above, the producer is in equilibrium, when the following two

conditions are fulfilled.

(1) The isoquant must be convert to

the origin.

(2) The slope of

the Isoquant must be equal to the slope of

isocost line.

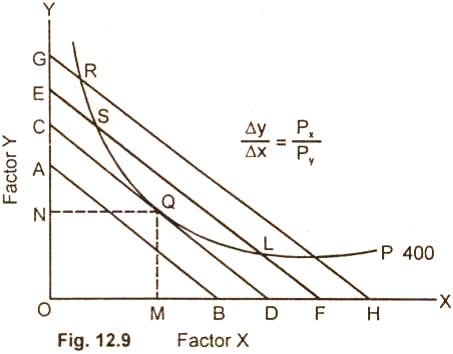

Diagram/Figure:

The least cost combination of

factors is now explained with the help of figure 12.9.

Here the isocost line CD is tangent

to the iso-product curve 400 units at point Q. The firm employs

OC units of factor Y and OD units of factor X to produce 400

units of output. This is the optimum output which the firm can

get from the cost outlay of Q. In this figure any point below Q

on the price line AB is desirable as it shows lower cost, but it

is not attainable for producing 400 units of output. As regards

points RS above Q on isocost lines GH, EF, they show higher

cost.

These are beyond the reach of the producer with CD outlay.

Hence point Q is the least cost point. It is the point which is

the least cost factor combination for producing 400 units of

output with OC units of factor Y and OD units of factor X. Point

Q is the equilibrium of the producer.

At this point, the slope of the

isoquants equal to the slope of the isocost line. The MRT of the

two inputs equals their price ratio.

Thus we find that at point Q, the

two conditions of producer's, equilibrium in the choice of

factor combinations, are satisfied.

(1) The isoquant (IP) is convex the

origin.

(2) At point Q, the slope of the

isoquant ΔY / ΔX (MTYSxy) is equal to the slope of

the isocost in Px / Py. The producer gets the optimum output at

least cost factor combination.

Relevant Articles:

|