Law of Supply:

Definition of

Law of Supply:

There is direct relationship between the price of a

commodity and its quantity offered fore sale over a specified period of time.

When the price of a goods rises, other things remaining the same, its quantity

which is offered for sale increases as and price falls, the amount available for

sale decreases. This relationship between price and the quantities which

suppliers are prepared to offer for sale is called the law of supply.

Explanation of Law of Supply:

The law of supply, in short, states that ceteris paribus sellers supply more goods at a

higher price than they are willing at a lower price.

Supply Function:

The supply function is now

explained with the help of a schedule and a curve.

Market Supply Schedule:

Market Supply Schedule of a Commodity:

(In Dollars)

|

Px |

4 |

3 |

2 |

1 |

| QxS |

100 |

80 |

60 |

40 |

In the table above, the produce are able and willing

to offer for sale 100 units of a commodity at price of $4. As the price falls,

the quantity offered for sale decreases. At price of $1, the quantity offered

for sale is only 40 units.

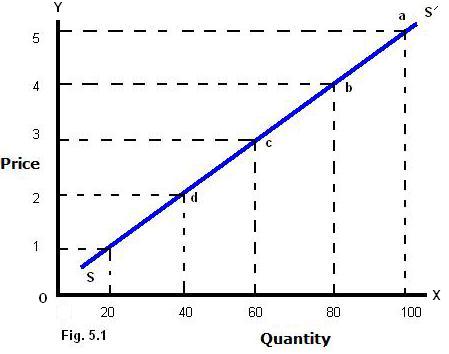

Law of Supply Curve/Diagram:

The market supply data of the commodity x as shown

in the supply schedule is now presented graphically.

In the figure (5.1) price is plotted on the vertical

axis OY and the quantity supplied on the horizontal axis OX. The four points d,

c, b, and a show each price quantity combination. The supply curve SS/

slopes upward from left to right indicating that less quantity is offered

for sale at lower price and more at higher prices by the sellers not supply

curve is usually positively sloped.

Formula for Law of Supply/Supply Function:

The supply function can also be expressed in

symbols.

QxS = Φ (Px

Tech, Si,

Fn, X,........)

Here:

Qxs = Quantity supplied of

commodity x by the producers.

Φ = Function of.

Px = Price of commodity x.

Tech = Technology.

S = Supplies of inputs.

F = Features of nature.

X = Taxes/Subsidies.

= Bar on the top of last four non-price factors

indicates that these variables also affect the supply but they are held constant.

Example of Law of Supply:

The law of supply is based on a moving quantity of

materials available to meet a particular need. Supply is the source of economic

activity. Supply, or the lack of it, also dictates prices. Cost of scarce supply

goods increase in relation to the shortages. Supply can be used to measure

demand. Over supply results in lack of customers. An over supply is often a

loss, for that reason. Under supply generates a demand in the form of orders, or

secondary sales at higher prices.

If ten people want to buy a pen, and there's only

one pen, the sale will be based on the level of demand for the pen. The supply

function requires more pens, which generates more production to meet demand.

Assumptions of Law of Supply:

(i) Nature of Goods. If the goods are

perishable in nature and the seller cannot wait for the rise in price. Seller

may have to offer all of his goods at current market price because he may not

take risk of getting his commodity perished.

(ii) Government Policies. Government may

enforce the firms and producers to offer production at prevailing market price.

In such a situation producer may not be able to wait for the rise in price.

(iii) Alternative Products. If a number of

alternative products are available in the market and customers tend to buy those

products to fulfill their needs, the producer will have to shift to transform

his resources to the production of those products.

(iv) Squeeze in Profit. Production costs like

raw materials, labor costs, overhead costs and selling and administration may

increase along with the increase in price. Such situations may not allow

producer to offer his products at a particular increased price.

Limitations/Exceptions of Law of Supply:

Exceptions that affect law of supply may include:

(i) Ability to move stock.

(ii) Legislation restricting quantity.

(iii) External factors that influence your industry.

Importance of Law of Supply:

(i) Supply responds to changes in

prices differently for different goods, depending on their

elasticity or inelasticity. Goods are elastic when a modest

change in price leads to a large change in the quantity

supplied. In contrast, goods are inelastic when a change in

price leads to relatively no response to the quantity supplied.

An example of an elastic good would be soft drinks, whereas an

example of an inelastic service would be physicians' services.

Producers will be more likely to want to supply more inelastic

goods such as gas because they will most likely profit more off

of them.

(ii) Law of supply is an economic

principle that states that there is a direct relationship

between the price of a good and how much producers are willing

to supply.

(iii) As the price of a good

increases, suppliers will want to supply more of it. However, as

the price of a good decreases, suppliers will not want to supply

as much of it. For producers to want to produce a good, the

incentive of profit must be greater than the opportunity cost of

production, the total cost of producing the good, which includes

the resources and value of the other goods that could have been

produced instead.

(iv) Entrepreneurs enter business ventures with the intention of

making a profit. A profit occurs when the revenues from the

goods a producer supplies exceeds the opportunity cost of their

production. However, consumers must value the goods at the price

offered in order for them to buy them. Therefore, in order for a

consumer to be willing to pay a price for a good higher than its

cost of production, he or she must value that good more than the

other goods that could have been produced instead. So supplier's

profits are dependent on consumer demands and values. However,

when suppliers do not earn enough revenue to cover the cost of

production of the good, they incur a loss. Losses occur whenever

consumers value a good less than the other goods that could have

been produced with the same resources.

Determinants of Supply:

There are four important

Determinants of Supply

as under:

(i) Technology changes.

Technology helps a producer to minimize his cost of

production.

(ii) Resource supplies. The producer also has to pay

for other resources such as raw materials and labor. if his

money is short on supplying a certain number of products

because of an increase in resource supplies, then he has to

reduce his supply.

(iii) Tax/ Subsidy. A

producer aims to maximize his profit, but an increase in tax

will only increase his expenses, decreasing his capacity to

buy resource supplies and forcing him to reduce his supply.

(iv) Price of other goods

produced. A producer may not only produce on product but

other products as well. A producer's money is limited and if

he increases his supply in one product, he would have to

decrease his supply in the other product, no unless his sales

increase.

Thus:

Qxs = Φ (Px)

Ceteris Paribus

Ceteris Paribus. In economics, the term is

used as a shorthand for indicating the effect of one economic variable on

another, holding constant all other variables that may affect the second

variable.

Relevant Articles:

|