Law of Constant Returns/Law

of Constant Cost:

(Version of Classical and Neo Classical

Economists):

Definition and Explanation:

The law of constant returns

also called law of constant cost. It is said to operate when with the

addition of successive units of one factor to fixed amount of

other factors, there arises a proportionate increase in total

output. The yield of equal return on the successive doses of

inputs may occur for a very short period in the process of

production. The law of constant return may prevail in those

industries which represent a combination of manufacturing as

well as extractive industries.

On the side of manufacturing

industries, every increased investment of labor and

capital may result in a more than proportionate increase in the

total output. While on the other extractive side, an increase in

investment may cause, in general, a less than proportionate

increase in the amount of produce raised. If the tendency of the

marginal return to increase is just balanced by the tendency of

the marginal return to diminish yielding an equal return, we

have the operation of the law of constant returns. In the words

of Marshall:

"If the actions of the law of increasing and

diminishing returns are balanced, we have the law of constant

return".

In actual life, the law of constant

returns can operate only if the following conditions are

fulfilled:

(i) There should not be any increase

in the prices of raw materials in the industry. This can only be

possible if commodities are available in large supply.

(ii) The prices of various factors

of production should remain the same. The .supply of various

factors of production needed for a particular industry should be

perfectly elastic.

(iii) The productive services should

not be fixed and indivisible.

If we study the above mentioned

conditions carefully, we will easily conclude that in the actual

world, it is not possible to find an industry which obeys the

law of constant returns. The law of constant returns can operate

for a very short period when the marginal return moves towards

the optimum point and begins to decline. If the marginal return,

at the optimum level remains the same with the increased

application of inputs for a short while, then we have the

operation of law of constant returns. The law is represented now in the form of a table and a

curve.

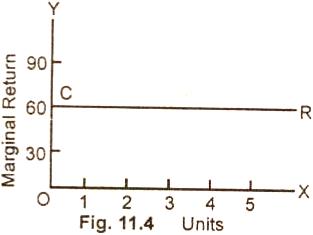

Schedule:

|

Productive doses

|

Total

Return (meters of cloth) |

Marginal

Return (meters of cloth) |

|

1 |

60 |

60 |

|

2 |

120 |

60 |

|

3 |

180 |

60 |

|

4 |

240 |

60 |

|

5 |

300 |

60 |

In the table given above, the

marginal return remains the same, i.e. 60 meters of cloth with

the increased investment of inputs.

Diagram/Graph:

In figure (11.4) along OX are

measured the productive resources and along OY is represented

the marginal return. CR is the fine representing the law of

constant returns. It is parallel to the base axis.

Relevant Articles:

|