Law of Costs:

Definition and Explanation:

Law of Costs is also

known as laws of returns. As an industry is expanded with the

increased investment of resources, the marginal cost (i.e., the

amount which is added to the total cost when the output is

increased by one unit) decreases in some cases, increases in

others and in some, it remains the same. This tendency on the

part of the marginal cost to fall, rise or to remain the same as

output is expanded, is described in economics as the law

of diminishing costs, the law of increasing costs, and the law

of constant costs.

If we know the money cost of a unit

of a factor invested in a particular industry, then the marginal

cost can be derived easily dividing the money cost of a unit of

factor by its marginal return.

The following table will make clear

as to how the marginal cost decreases with the increases in

marginal returns, rises with the fall in marginal returns and

remains constant with the marginal return remaining the same.

Let us suppose that the cost of each unit of factor applied is

worth $100 only.

Schedule:

|

Units of Factor

|

Total Return

(meters of Cloth)

|

Marginal Return (meters)

|

Marginal Cost (in Dollars) (per meter) |

|

1 |

10 |

10 |

10 |

|

2 |

30 |

20 |

5 |

|

3 |

55 |

25 |

4 |

|

4 |

88 |

33 |

3 |

|

5 |

138 |

50 |

2 |

|

6 |

238 |

100 |

1 |

|

7 |

338 |

100 |

1 |

|

8 |

400 |

62 |

1 |

|

9 |

450 |

50 |

2 |

|

10 |

475 |

25 |

4 |

|

11 |

490 |

15 |

6 |

In the schedule given above, the taw

of diminishing costs operates up to the 6th unit, between the

6th and 7th units, it is the law of constant costs which

prevails and from 7th unit onward, it is the law of increasing

costs which sets in.

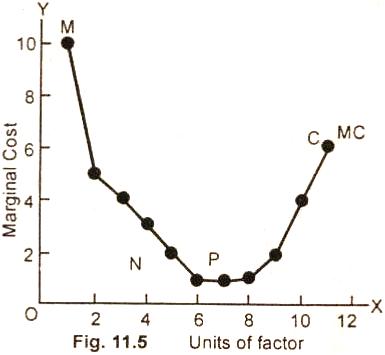

Diagram/Graph:

In the Fig. (11.5) units of factors

are measured along OX axis and marginal cost along OY axis. The

failing curve MN represents the operation of law of

diminishing costs. NP shows constant costs, and PC indicates the

increasing cost. MC is the marginal cost curve.

Relevant Articles:

|