Law of Increasing Returns/Law

of Diminishing Cost:

(Version of Classical and Neo

Classical Economists):

Definition and Explanation:

The law of increasing returns

is also called the law of diminishing costs. The law of

increasing return states that:

"When more and more units of a

variable factor is employed, while other factor remain fixed,

there is an increase of production at a higher rate. The

tendency of the marginal return to rise per unit of variable

factors employed in fixed amounts of other factors by a firm is

called the law of increasing return".

An increase of variable factor,

holding constant the quantity of other factors, leads generally

to improved organization. The output increases

at a rate higher than the rate of increase in the employment of

variable factor.

The increase in output faster than

inputs continues so long as there is not deficiency of an

essential factor in the process of production. As soon as there

occurs shortage or a wrong or defective combination in

productive process, the marginal product begins to decline. The

law of diminishing return begins to operate. We can, therefore,

say that there are no separate laws applicable to agriculture

and to industries. It is only the law of variable proportions

which applies to a!! the different industries. However, the

duration of stages in each productive undertaking will vary.

They will depend upon the availability of resources, their

combination in right proportions, etc., etc.

Application of the Law of Increasing

Returns in Industries:

There are certain manufacturing

industries where the factors of production can be combined and

substituted up to a certain limit, it is the law of increasing

returns which operates. In the words of Prof. Chapman:

"The expansion of an industry in

which there is no dearth of necessary agents of production tends

to be accompanied, other things being equal, by increasing

returns".

The increasing returns mainly arises

from the fact that large scale production is able to secure certain economies of

production, both internal and external. When an industry is

expanded, it reaps advantages of division of labor, specialized

machinery, commercial advantages, buying and selling wholesale,

economies in overhead expenses, utilization of by products, use

of extensive publicity and advertisement, availability of cheap

credit, etc.. etc.

The law of increasing returns also

operates so long as a factor consists of large indivisible units

and the plant is producing below its capacity. In that case,

every additional investment will result in the increase of

marginal productivity and so in lowering the cost of production

of the commodity produced. The increase in the marginal

productivity continues till the plant begins to produce to its

full capacity.

Assumptions:

The law rests upon the following

assumptions:

(i) There is a scope in the

improvement of technique of production.

(ii) At least one factor of

production is assumed to be indivisible.

(iii) Some factors are supposed to

be divisible.

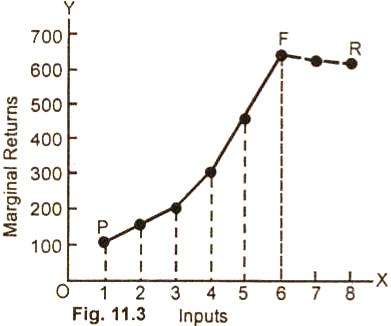

Example:

The law of increasing returns can

also be explained with the help of a schedule and a curve.

Schedule:

|

Inputs |

Total

Returns (meters of cloth)

|

Marginal

Returns

(meters of cloth)

|

|

1

|

100

|

100

|

|

2

|

250

|

150

|

|

3

|

450

|

200 |

|

4

|

750

|

300

|

|

5

|

1200

|

450

|

|

6

|

1850

|

650

|

|

7 |

2455 |

605

|

|

8

|

3045

|

600

|

In the above table it is dear that

as the manufacturer goes on expanding his business by investing

successive units of inputs, the marginal return goes on

increasing up to the 6th unit and then it beings to decline

steadily, Here, a question ca be asked as to why the law of

diminishing returns has operated in an industry?

The answer is very simple. The

marginal returns has diminished after the sixth unit because of

the non-availability of a factor or factors of production or.

the size of the business has become so large that it has become unwieldy to manage it, or

the plant is producing to its full capacity and it is not

possible further to reap the economies of large scale

production, etc., etc.

Diagram/Graph:

In figure 11.3, along OX axis are

measured the units of inputs applied and along OY axis the

marginal return is represented. PF is the curve representing the

law of increasing returns.

Compatibility of Diminishing and Increasing Returns:

It is often pointed out by the

classical economists that the law of diminishing returns is

exclusively confined to agriculture and other extractive

industries, such as mining fisheries, etc. while manufacturing

industries obey the law of increasing returns. In the words of

Marshall:

"While the part which Nature plays

in production shows a tendency to diminishing returns and the

part which man plays shows a tendency to increasing returns".

The modern economists differ with

this view and are of the opinion that the law of diminishing

returns applies both to agriculture and the industry. The only

difference is that in agriculture the law of diminishing returns

begins to operate at an early stage and in an industry somewhere

at a later stage.

The law of increasing returns is

also named as the Law of Diminishing Cost. When the addition to

output becomes larger, as the firm adds successive units of a

variable input to some fixed inputs, the per unit cost begins to

decline. The tendency of the cost per unit to decline with

increased application of a variable factor to fixed factors is

called the Law of Diminishing Cost.

Relevant Articles:

|