Law of Returns to Scale:

Definition and Explanation:

The law of returns are often

confused with the law of returns to scale. The law of

returns operates in the short period. It explains the production

behavior of the firm with one factor variable while other

factors are kept constant. Whereas the law of returns to

scale operates in the long period. It explains the production

behavior of the firm with all variable factors.

There is no fixed factor of

production in the long run. The law of returns to scale

describes the relationship between variable inputs and output

when all the inputs, or factors are increased in the same

proportion. The law of returns to scale analysis the effects of

scale on the level of output. Here we find out in what

proportions the output changes when there is proportionate

change in the quantities of all inputs. The answer to this

question helps a firm to determine its scale or size in the long

run.

It has been observed that when there

is a proportionate change in the amounts of inputs, the behavior

of output varies. The output may increase by a great proportion,

by in the same proportion or in a smaller proportion to its

inputs. This behavior of output with the increase in scale of

operation is termed as increasing returns to scale, constant

returns to scale and diminishing returns to scale. These three

laws of returns to scale are now explained, in brief, under

separate heads.

(1) Increasing Returns to Scale:

If the output of a firm increases

more than in proportion to an equal percentage increase in all

inputs, the production is said to exhibit increasing returns to

scale.

For example, if the amount of

inputs are doubled and the output increases by more than double,

it is said to be an increasing returns returns to scale. When

there is an increase in the scale of production, it leads to

lower average cost per unit produced as the firm enjoys

economies of scale.

(2) Constant Returns to Scale:

When all inputs are increased by a

certain percentage, the output increases by the same percentage,

the production function is said to exhibit constant returns to

scale.

For example, if a firm

doubles inputs, it doubles output. In case, it triples output.

The constant scale of production has no effect on average cost

per unit produced.

(3) Diminishing Returns to Scale:

The term 'diminishing' returns to

scale refers to scale where output increases in a smaller

proportion than the increase in all inputs.

For example, if a firm

increases inputs by 100% but the output decreases by less than

100%, the firm is said to exhibit decreasing returns to scale.

In case of decreasing returns to scale, the firm faces

diseconomies of scale. The firm's scale of production leads to

higher average cost per unit produced.

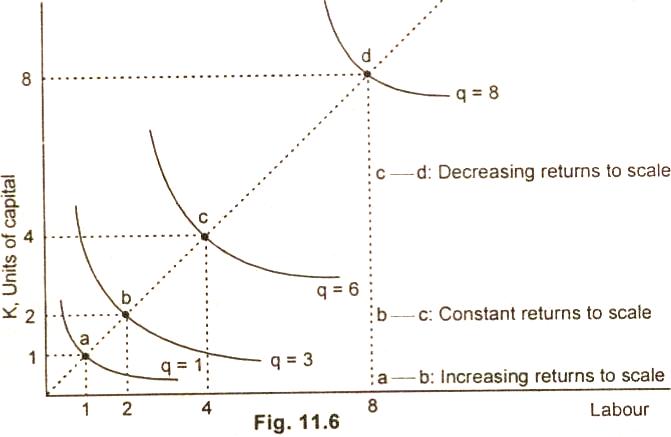

Graph/Diagram:

The three laws of returns to scale

are now explained with the help of a graph below:

The figure 11.6 shows that when a

firm uses one unit of labor and one unit of capital, point a, it

produces 1 unit of quantity as is shown on the q = 1 isoquant.

When the firm doubles its outputs by using 2 units of labor and

2 units of capital, it produces more than double from

q = 1 to q = 3.

So the production function has

increasing returns to scale in this range. Another output from

quantity 3 to quantity 6. At the last doubling point c to point

d, the production function has decreasing returns to scale. The

doubling of output from 4 units of input, causes output to

increase from 6 to 8 units increases of two units only.

Relevant Articles:

|