|

Economics Concepts A free website that explains economics with amazing clarity www.economicsconcepts.com |

|

|

2011 Master Accounting Download Package Only For $35 |

| Home Page Contact Us About Us Privacy Policy Terms of Use Advertise Links |

Market Price:Definition of Equilibrium:In a market, there are two sets of forces tending in the opposite direction. On the one side, there are large number of buyers who compete with one another for the purchase of commodities at lower prices. Competition amongst the buyers tends to raise the price. On the other side, there are large number of sellers who compete with one another for the, sale of commodities at higher prices. Competition amongst the sellers tends to lower the price. When the pressure of these two forces is equal in the opposite direction, i.e., when the quantity offered for sale is just equal the quantity demanded at a particular price, the market is said to be in equilibrium.

Definition of Market Price:

The price at which the amounts demanded and supplied is exactly equal, is. called the market price.

Explanation:

The market equilibrium or the market price is not something fixed. It is subject to fluctuations with the increase or decrease in demand or with the increase or decrease in supply. Market price or the very short run price is the price which tends to prevail in the market at any particular, time. It may change from hour to hour or from day to day. It is, in fact, the result of temporary equilibrium, between the demand for and the supply of a commodity at a certain time, e.g., if the demand for a commodity increases per unit of time, supply remaining the same, prices go up. We can, thus, call the market price as the changing equilibrium.

When the period is very short, say an hour, or, a few hours, the supply of the commodities if demanded more cannot be increased with the further production of goody. The supply can only be brought from the stock already available for sale. In a very short period, the cost of production has a very negligible influence on the market price. If the commodities are perishable, like fish, fruits, etc., and there is no arrangement available for placing them in cold storages, then the cost of production has practically no influence on price and there is also no reserve-price on the part of the sellers.

If the commodities can be kept for a longer period, then it has an indirect influence on market price. If price falls lower than the reserve price, the commodities will not be brought for sale but will be kept in store hoping to dispose them off when their prices cover the cost of production. The analysis of the market equilibrium or the market price stated above can be discussed in more detail.

(1) Market Price of Perishable Commodities:

In a case of a commodity which, is perishable, the cost of production has practically no influence on the market price. The whole of the stock has to be disposed off at the prevailing price. Let us suppose a perishable commodity like fish is brought for sale in the market to the amount of 50 kilograms. The total quantity of fish demanded by all individuals in the market at various prices per day is as follows:

Schedule:

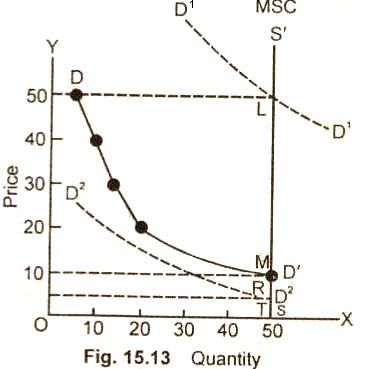

From the schedule given above, the reader can understand that if the seller wishes to sell the whole of the stock, it can be sold at $10 per kilogram. As in a perfect market, there can be only one price for a particular commodity, so the buyers who are willing to buy at higher price, enjoy consumer's surplus. The price determination in the market period can be illustrated with the help of a diagram. The equilibrium market price is where demand and supply curves intersect.

Diagram/Graph:

In the graph (15.13) quantity is measured along OX axis and price along OY axis. As the supply of a perishable commodity is fixed and cannot be held back, therefore, the market period supply curve (MSC). SS will be a vertical straight line. The market demand curve DD' intersects the market supply curve at point M. MS ($10) is the market price at which the total quantity of fish is sold in the market.

Let us suppose that demand for fish rises due to strike on the part of the meat sellers, the new demand curve D1D1 intersects the market supply curve at point LLS which is equal to $50 will be new market price. If the demand falls, the new demand curve D2D2 cuts the supply curve at point R. $30 which is equal to $5 is the new equilibrium price.

(2) Market Price of Non-Perishable Commodities:

When the commodities are not perishable, the stock can be kept in store for certain period. If prices rise and the sellers think it profitable to sell, then the whole of the stock can be brought in the market for sale. If prices fall and the sellers do not think it advantageous to sell, then a part or whole of the stock can be withheld with a view to sell it at some future date when the prices rise. After haggling and bargaining, a price is established which just clears the market. At this price, the total amount demanded is exactly equal to the total amount supplied. This can be proved with the help of a schedule and a diagram.

Schedule:

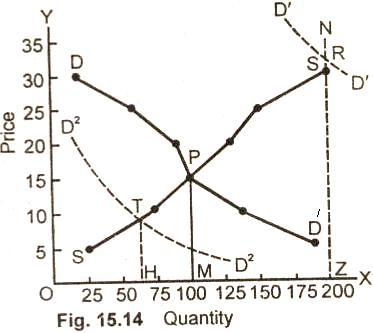

In the schedule given above, when the price of a commodity is $15 per quintal, the total, quantity demanded per week is just equal to the total quantity supplied, i.e., 100 quintals.

Diagram:

It can also be illustrated with the help of a diagram. In the Fig. (15.14) SSN is the supply curve of non-perishable commodity in the very short period. OZ is the quantity of goods which can be brought into the market for sale. DD/ is the market demand curve which intersects the market. supply curve at point P. PM which is equal to $15 is the equilibrium price or the market price point P. PM which is equal to $15 is the equilibrium price or the market price and OM the equilibrium amount If the demand rises, the new market demand curve intersects the supply curve at point R. RZ then will be the, market price. NS position of the supply curve is a vertical line showing that even if price rises, the quantity cannot be increased. However, the price will go up with the increase in demand.

If the demand falls, the new demand curve D2D2 cuts. The supply curve at point T. TH then is the market price. It shows that at lower price, less commodity is offered for sale. In this case, it is OH quantity only which is brought into the market for sale at TH price.

|

Home Page Contact Us About Us Privacy Policy Terms of Use Advertise Links

All rights reserved Copyright ©2011