Determination of Short Run Normal Price

of Firm and Industry:

Definition:

In the short run, the size of a firm

and the number of firms comprising an industry remain the same.

The time is considered to be so short that if demand for product

increases, the old firm can use their existing equipments more

intensively but new firms cannot enter into the industry. The

short run normal price is established at a point where the short

period supply curve and the demand curve intersect each other.

The

short run supply curve of the industry is the lateral

summation of the short period marginal cost curves of all the

firms. While the market demand curve is a falling curve

indicating that more is bought when price is low and less when

price is high.

Explanation:

The determination of price and

output in the short run can be explained with the help of the

above diagrams.

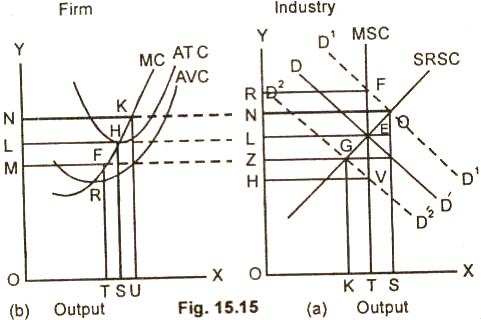

Diagram/Figure:

In the fig. 15.15(a) the short run

supply curve (SRSC) of the industry intersects the market demand

curve at point E. The price will be OL and the quantity supplied

OT.

We suppose now that the demand for

the commodity has gone up. The new demand curve D1D1

intersects the market supply curve (MSC) at point F. The price

rise from OL to OR without affecting the output which remains OT

as before. The entrepreneur lured by higher prices will use the

fixed capital equipment more intensively. The old machines will

also be repaired and the production expanded. The new demand

curve then intersects the short period supply curve SRSC at

point Q.

In fig 15.15(b) ON will be the short run normal price which is higher

than the original market price OL but lower than the raised

market price OR. ON thus is the short run normal price of an

industry. This price cannot be changed by the action of an

individual firm as it produces an insignificant portion of the

total supply of the output. It will have to adjust its product

accordingly. At price ON, the firm is earning abnormal profits

because the price is higher than the normal price OL.

If the market demand falls, the new

demand curve D2D2 intersects the market

period supply curve at point G. OZ then is the new equilibrium

market price which is lower than the original OL market price.

The fall in the market price will affect the supply of the

commodity. The firms will reduce their output by decreasing the

variable factors.

Relevant Articles:

|