Equilibrium of the Firm

Under Perfect Competition

or

Marginal Revenue = Marginal Cost (MR = MC) Rule:

Definition and Explanation:

A firm under

perfect

competition faces an infinitely elastic demand curve or we

can say for an individual firm, the price of the commodity is

given in the market. The firm while making changes in the

amounts of variable factor evaluates the extra cost incurred on

producing extra unit MC (Marginal

Cost).

It also examines the change in total receipts which

results from the sale of extra unit of production MR (Marginal

Revenue). So long as the additional revenue from the sale of

an extra unit of product (MR) is greater than the additional

cost (MC) which a firm has to incur on its production, it will

be in the interest of the firm to increase production.

In economic terminology, we can say,

a firm will go on expanding its output so long as the marginal

revenue of any unit is greater than its marginal cost. As

production increases, marginal cost begins to increase after a

certain point. When both marginal revenue and marginal cost are

equal, the firm is in equilibrium. The firm at this equilibrium

point is cither ensuring maximum profit or minimizing losses.

This is shown with the help of a diagram below:

Diagram/Figure:

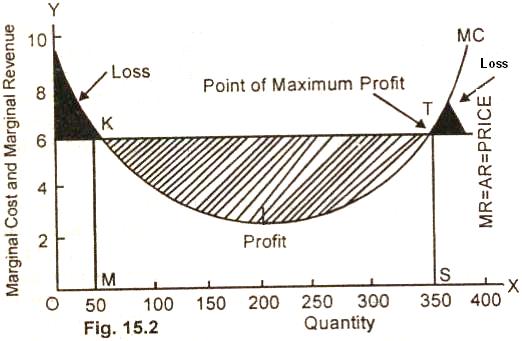

In the figure (15.2) quantity of

output is measured along OX axis and marginal cost and marginal

revenue on OY axis. The marginal cost curve cuts the marginal

revenue curve at two points K and T.

The competitive firm is in

equilibrium, at both these points as marginal cost equals

marginal revenue. The firm will not produce OM quantity of good

because for OM output, the marginal cost is higher than marginal

revenue. Marginal cost curve cuts the marginal revenue curve

from above. The firm incurs loss equal to the black shaded area

for producing 50 units (OM) of output.

As production is increased from 50

units to 350 units (from OM to OS) marginal cost decreases at

early levels of output and then increases thereafter. The

marginal cost curve cuts the marginal revenue curve from below

at point T. The shaded portion between M to S level of output

shows profit on production. When a firm produces OS quantity of

output; it earns maximum profit. The point T where MR = MC is

the point of maximum profit.

In case, the firm increases the

level of output from OS, the additional output adds less to Its

revenue than to its cost. The firm undergoes losses as is shown

in the shaded area.

Summing up, profit

maximization normally occurs at the rate of output at which

marginal revenue equals marginal cost. This golden rule holds

good for all market structures. As regards the absolute profits

and losses of the firm, they depend upon the relation between

average cost and

average revenue

of the firm.

Relevant Articles:

|